RISK MANAGEMENT AND OPPORTUNITIES: AT A GLANCE

How We Manage Risk.

ERM is integrated into strategy and operations, guiding which projects we pursue, how we invest, and how we run our assets day to day.

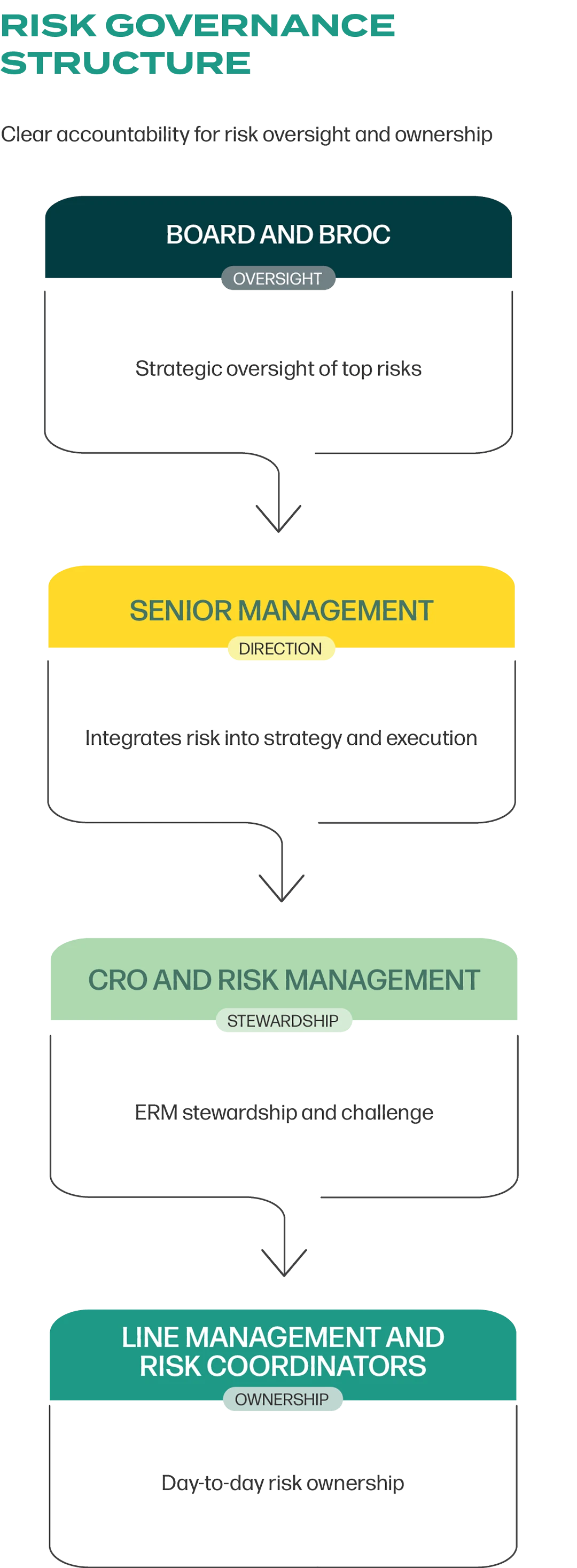

Who Owns Which Risks.

The Board, Senior Management, the Chief Risk Officer (CRO), the Risk Management Department, and line managers each have defined roles so risks are owned, escalated, and acted on.

What Risks Are Critical.

The same six risk categories apply as last year—policy and transition, fuel supply, climate, infrastructure, finance, and cybersecurity—but the nature of our exposure has shifted as First Gen moves toward a renewable portfolio.

How We Respond.

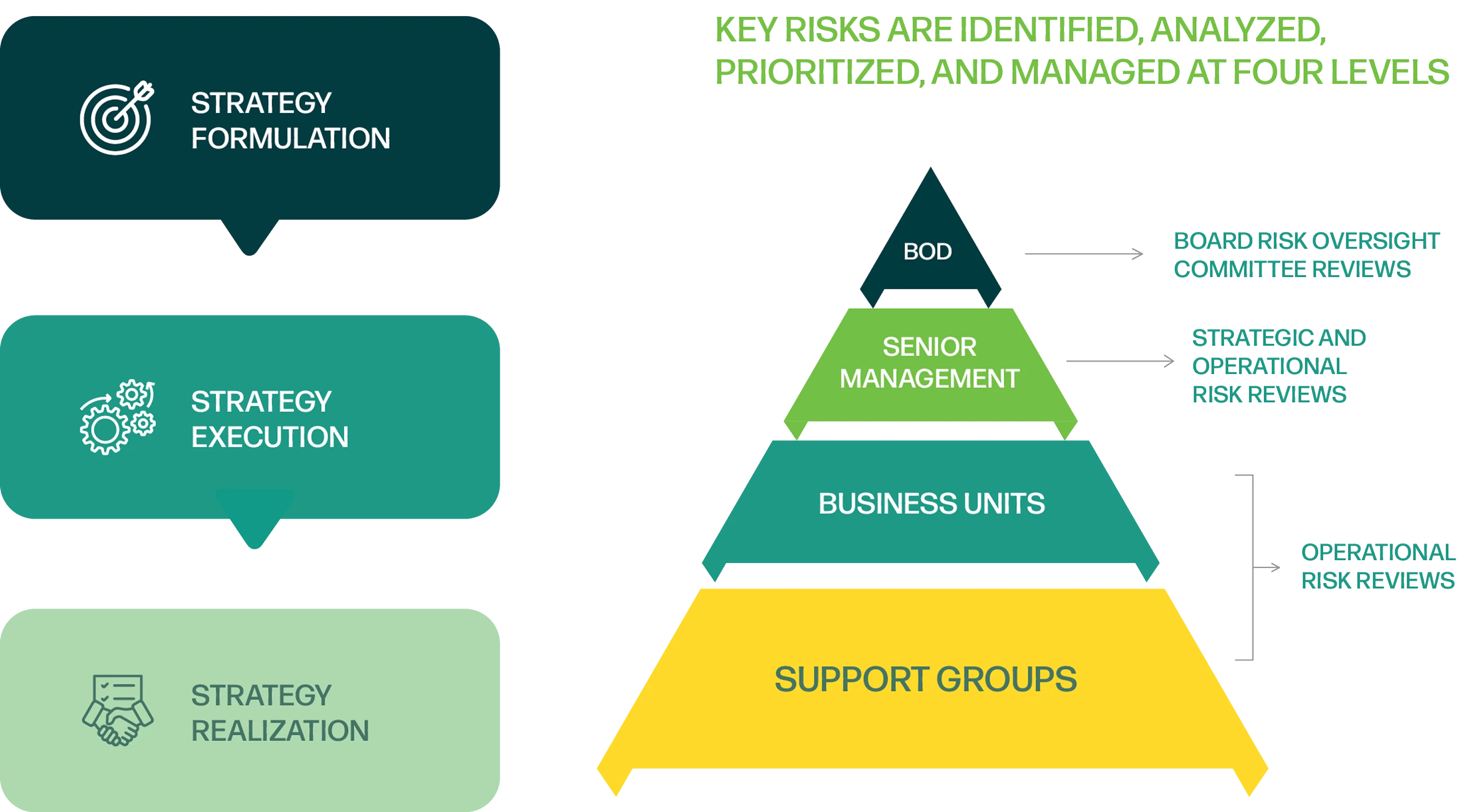

Risk assessments are conducted on a regular basis across three levels: Strategy, Operations (including Support Groups), and Projects. We implemented a cloud-based solution to record potential issues and mitigating strategies, including the monitoring of their implementation and completion.

Where We See Opportunity.

The opening of the retail market and the growing competitive advantage of renewable power are opportunities First Gen has been preparing for, but capturing them depends on the enabling environment keeping pace with the transition.

Managing Risk in our Renewable Energy Transition

First Gen is reallocating capital from natural gas assets toward a larger, more diverse portfolio of renewable energy projects in the Philippines and abroad. This shift changes the Company’s risk profile—across policy and transition, fuel supply, climate, infrastructure, finance-related, and cybersecurity risks—but also opens space to build a more resilient, renewable portfolio.

Growing a renewable portfolio with new partners calls for a clear roadmap of where value could be lost—and created—across the business. Our framework ties risk identification, assessment, and mitigation to the decisions that matter most. The Enterprise Risk Management (ERM) process runs through our value-creation activities, from business units and project teams to support groups.

Clear Roles Matter

Clear roles ensure that risks are surfaced, discussed at the right level, and translated into concrete actions.

- Board Risk Oversight Committee (BROC): The BROC sets direction for how First Gen manages its most important strategic risks and checks that management has the mandate and resources to act. It receives regular updates on top risks and mitigation effectiveness.

- Senior Management: They assist the BROC in its supervisory role and lead the rollout of the ERM system within individual departments. At the project level, the GRAC applies a risk overlay to major project and capital decisions—surfacing key risks as an additional input before commitments are made. Beginning in 2026, the Sustainability Steering Committee will set strategic direction on sustainability, with material sustainability risks as a direct input to that process.

- Chief Risk Officer (CRO) and Risk Management Department: The CRO holds ultimate responsibility for a strong, organization-wide ERM system. The Risk Management Department stewards the framework, maintains the cloud-based risk register, and ensures continuous refinement.

- Line Management and Risk Coordinators: Line managers are risk owners entrusted with identifying, assessing, and managing risks in their specific domains. Risk coordinators tasked per group consolidate data for the cloud-based register.

![]()

Strategic risks are incorporated into Strategic Board Updates as agreed with the BROC Chairman. The strategic and operational risks of business groups are reviewed by Senior Management and presented to the BROC. Project and operating asset risks are reviewed and updated quarterly, and presented to Senior Management and the BROC annually. Support-group risks are reviewed semi-annually and reported to the CRO annually.

How We Identify, Assess, and Review Risks

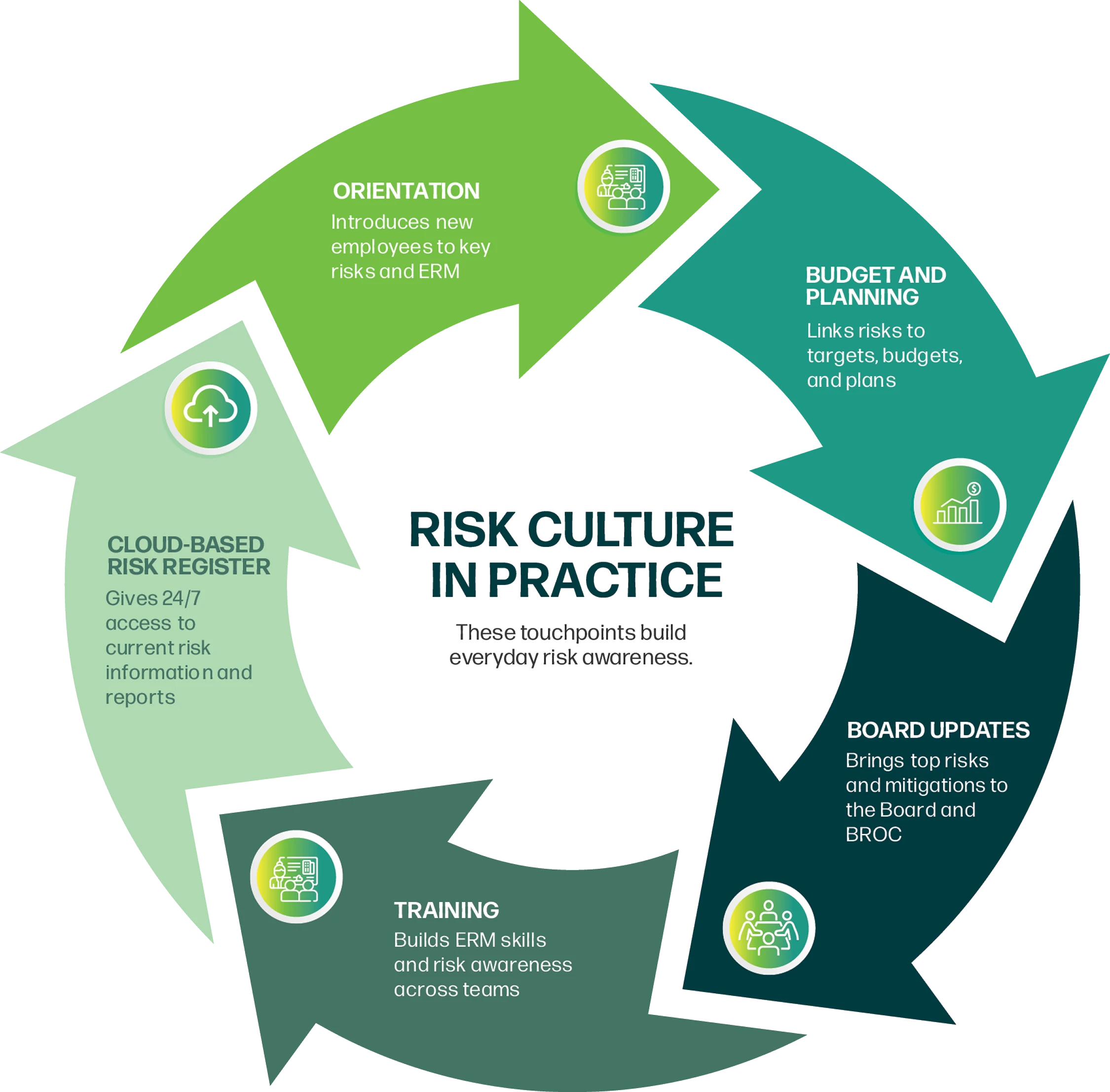

Risk identification starts where the work happens. Risk owners—together with the Risk Management Group—surface issues, analyze the likelihood and its impact, and, if any, strategize mitigating measures and monitor its implementation. In 2025, Risk Management shifted from manual, spreadsheet‑based registers to a cloud‑based risk register, giving authorized users 24/7 access and automated reporting to keep data accurate and decision‑ready. Review frequencies are matched to the nature of risks.

- Strategic Risks: Identified and monitored by Senior and Line Management; presented to the BROC annually

- Project and Operating Asset Risks: Reviewed and updated quarterly; presented to Senior Management and the BROC annually

- Support-Group Risks: Reviewed semi-annually and reported to the CRO annually

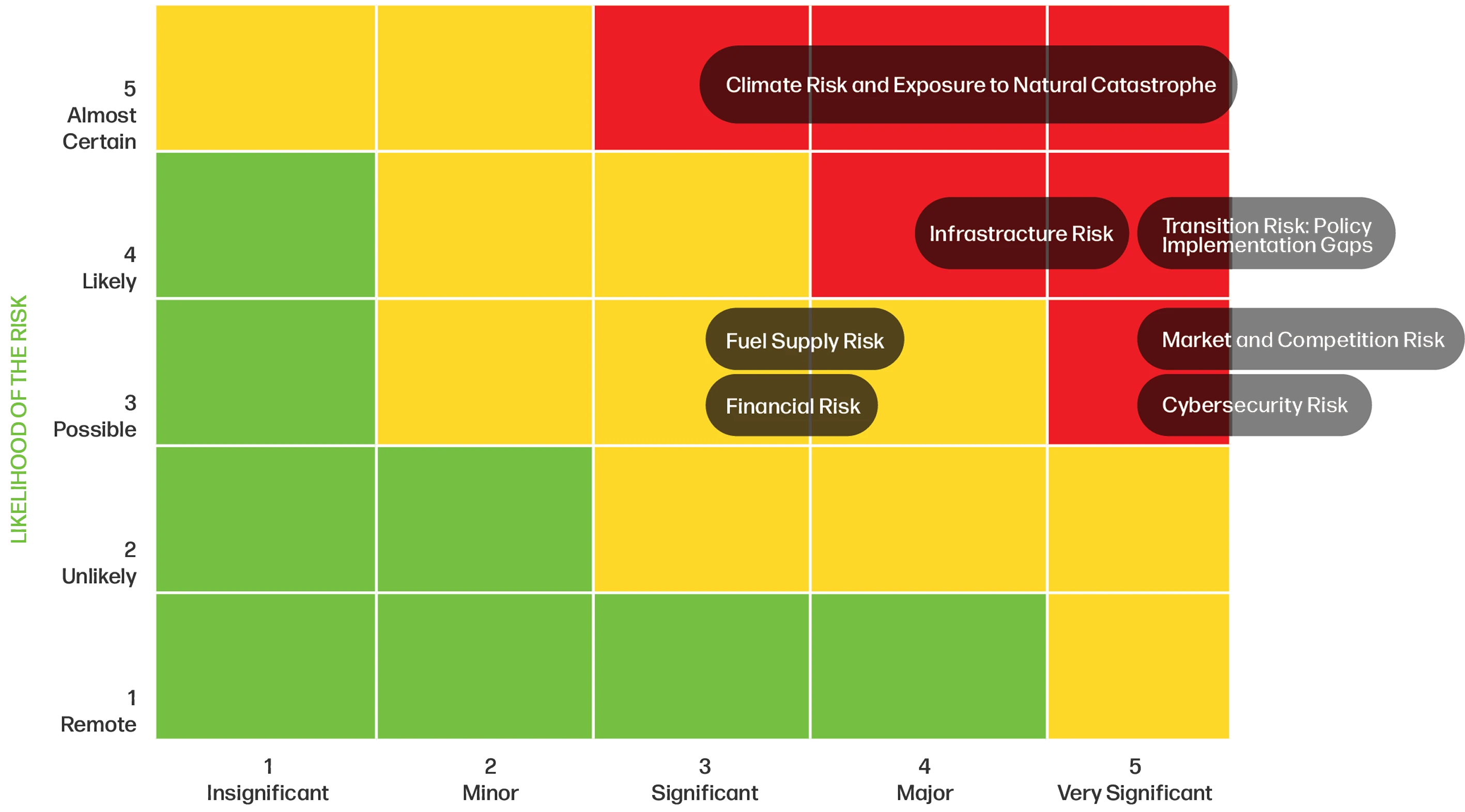

Key Risks in a Transitioning Portfolio

First Gen has identified the key risks the Company may face based on comprehensive assessments. The heat map illustrates the inherent impact and likelihood of these risks, providing a concise visual overview of potential threats to the achievement of our objectives.

The succeeding table presents a more detailed discussion of each identified risk, its relevance to the Company, and its potential effects on our capitals and stakeholders. It also outlines how these risks may influence our strategic direction, together with the corresponding mitigation measures and the expected outcomes of these actions.

As First Gen shifts toward a portfolio led by renewables and retail exposure, the shape of our risk profile is evolving.

KEY RISKS:

Transition Risk: Policy Implementation Gaps

The Philippines has built a strong policy foundation for clean energy—through the Renewable Portfolio Standards, Green Energy Auction, net metering, the Green Energy Option Program, and the progressive opening of retail competition under RCOA. The challenge is not ambition; it is the pace at which these mechanisms translate into actual clean generation. For First Gen, the risk is specific: delays in or modified implementation of such policies affects the viability and timing of investment in both existing and new renewable assets.

Risk Type: External

Capitals Affected and Direct and Indirect Impacts

- Financial—Delays can prolong the pursuit or achievement of company targets and plans.

- Social & Relationship—Delays in investment and project timelines may strain relationships with regulators, communities, and partners who depend on First Gen’s clean energy commitments being realized.

- Manufactured—Delayed or deferred investment means the physical asset base does not grow as planned, limiting the productive capacity of First Gen’s renewable portfolio and increasing the cost of catching up.

- Natural—Clean energy projects that are delayed or deferred due to policy uncertainty mean indigenous renewable resources remain untapped and the environmental benefit of clean generation is not realized.

Stakeholders Affected by or Involved in Risk Management

- Customers—Slower renewable deployment prolongs dependence on conventional generation that relies on imported fuel, potentially exposing customers to volatile electricity prices.

- Regulators—The DOE, ERC, and other regulatory bodies are active partners in closing policy implementation gaps.

- Host communities—Delays in new renewable projects slow the delivery of local economic benefits, including employment, livelihood programs, and energy revenues.

Likelihood of the Risk Occuring: Likely

Magnitude of the Impact on the Company: Major

Time Horizon: Medium to Long Term

Effects on Strategic Objectives and Key Targets

- Delays in regulatory implementation may slow the achievement of First Gen’s clean energy growth targets.

- Less supportive market conditions may affect the financial viability of existing assets and new renewable investments.

Mitigation Measures

- Public Advocacy Capability—First Gen is developing CEAL, the organizational capability to engage constructively with industry peers and civil society to advance the clean energy transition.

- Direct Regulatory Engagement—First Gen participates in technical working groups with the DOE, ERC, and other regulatory bodies in the development of key issuances.

- Coalition Building—First Gen collaborates with like-minded organizations and customer groups to advance clean energy market development.

What these Measures Achieve

Constructive engagement with the policy process reduces First Gen’s exposure to implementation delays and helps ensure the regulatory environment continues to move toward the Philippines’ clean energy commitments.

Market and Competition Risk

Fossil fuel generation continues to dominate the energy mix. Procurement decisions that prioritize upfront cost—without accounting for the environmental cost of carbon emissions—continue to give fossil fuel generators price advantage over renewables. The opening of RCOA Phase 4 in June 2026 adds another dimension—bringing both competitive pressure and strategic opportunity simultaneously.

First Gen’s roots lie in traditional wholesale power production and supply, a legacy position that creates real exposure as the market restructures. The Company has been preparing for this shift. The establishment of the Revenue Office and Customer Engagement Office, the acquisition of Pi Energy, and the integration of a retail platform ahead of the market opening, in particular, are concrete steps in that direction.

Risk Type: External

Capitals Affected and Direct and Indirect Impacts

- Human—Managing a larger and more diverse retail customer base requires capabilities still being developed at First Gen.

- Financial—Failure to establish retail market position or recontract expiring capacities may result in revenue decline.

- Social & Relationship—Failure to establish strong customer relationships, in both the captive and contestable markets, weakens trust and partnerships that First Gen depends on.

- Manufactured—Plant capacity may be underutilized if customer contracts are not secured.

Stakeholders Affected by or Involved in Risk Management

Customers—Failure to establish a strong retail presence means customers lose access to competitively priced clean energy. If the market does not transition at pace, customers remain exposed to the price volatility that comes with dependence on imported fuel.

Likelihood of the Risk Occuring: Possible

Magnitude of the Impact on the Company: Significant

Time Horizon: Short to Medium Term

Effects on Strategic Objectives and Key Targets

- Failure to recontract existing generation capacities affects revenue and the financial performance.

- Failure to grow and retain retail customers across all market segments may limit First Gen’s long-term competitiveness.

- Underperformance in either market—captive or contestable—slows the expansion of First Gen’s clean energy portfolio.

Mitigation Measures

- Customer Engagement Capability—First Gen seeks to build Solutions-Based Customer Engagement (SBCE) as a core organizational capability and to move beyond commodity power supply to offering integrated energy solutions grounded in deep customer insight.

- Sales and Recontracting—Developing focused sales and marketing strategies will help First Gen prospect and recontract across all customer segments.

- Organizational Readiness—Establishing the Revenue Office and Customer Engagement Office, acquiring Pi Energy, and building back-office operations capable of serving both retail and wholesale markets maintain First Gen’s responsiveness.

What These Measures Achieve

These measures position First Gen to compete effectively in both the captive market—served through distribution utilities and electric cooperatives—and the growing contestable retail market. Recontracting secures the existing revenue base while retail capability builds the foundation for growth as more customers gain the power to choose their supplier.

Climate-Related Risks and Exposure to Natural Catastrophes

The extreme weather events and shifting rainfall patterns described in our Business Environment section are evidence of intensifying climate change—not isolated incidents. For First Gen, whose generation depends entirely on natural systems, this translates directly into operational risk: unpredictable rainfall affects hydro output and geothermal reservoir recharge, while extreme weather threatens asset integrity across operating sites. These risks affect our ability to deliver reliable clean energy and sustain the financial performance our stakeholders depend on.

Risk Type: External

Capitals Affected:

- Financial—Extreme weather events increase costs caused by asset repairs, generation losses, and higher insurance premiums—affecting revenue and financial performance.

- Manufactured—Physical assets are exposed to damage from typhoons, flooding, and seismic events, reducing generation capacity and requiring costly rehabilitation.

- Human—Extreme weather affects the health, safety, and mobility of employees and contractors at operating sites, reducing workforce availability and productivity during and after disruptions.

- Social and Relationship—Extreme weather events directly damage the homes and livelihoods of communities near our operating sites. How First Gen responds, standing alongside communities in recovery, can either erode or deepen the trust and partnership value built over time.

Stakeholders Affected by or Involved in Risk Management

- Customers—Severe weather events can disrupt power generation and affect the reliability of power supply, limiting access to the clean energy customers depend on.

- Employees and Contractors—Personnel at operating sites are directly exposed to extreme weather events. Emergency preparedness programs and regular drills are designed to ensure their safety and enable a coordinated response when disruptions occur.

- Host Communities—Communities near our operating sites participate in emergency preparedness planning and resilience programs alongside First Gen, making them active partners in managing climate risk.

Likelihood of the Risk Occuring: Almost Certain

Magnitude of the Impact on the Company: Significant

Time Horizon: Medium to Long Term

Effects on Strategic Objectives and Key Targets

- Damage to power assets reduces generation capacity and diverts capital from portfolio growth to rehabilitation, setting back First Gen’s clean energy ambition.

- Unmanaged physical climate risks increase the cost and complexity of developing new renewable projects.

- Climate events that harm vulnerable host communities undermine First Gen’s commitment to building resilient communities—a key focus area under Total Stakeholder Value.

Mitigation Measures

- Governance—GRAC evaluates project proposals’ climate-related risks before major capital commitments are approved. Beginning in 2026, the Sustainability Steering Committee brings physical climate risks into strategic direction-setting as an input to the planning process.

- Organizational Capability—Building Agile Multi-Project Development (AMPD) and Resilient Asset Management (RAM) gives First Gen the core capabilities needed to deliver projects and manage assets under changing climate and regulatory conditions.

- Physical Risk Assessment—First Gen conducts natural calamity studies covering typhoons, floods, tsunamis, and earthquakes and continuously updates with additional data providers to keep climate risk information current.

- Asset Resilience—First Gen continuously modifies plant design and implements weather-proofing and resilience initiatives, while also installing seismic monitors at strategic locations across operating sites.

- Emergency Preparedness—Emergency response and business continuity management plans across operating sites undergo continuous review alongside regular drills to test readiness.

- Community Resilience—First Gen plans to integrate community climate resilience into its sustainability programs, supporting host communities in preparing for and recovering from extreme weather events.

- Risk Transfer—First Gen obtains and maintains natural catastrophe insurance coverage across key sites.

- Risk Awareness—Training programs foster risk appreciation across teams and operating sites.

What These Measures Achieve

These measures protect the physical foundation of First Gen’s

clean energy generation—keeping assets operational, sustaining reliable power supply to customers, safeguarding the health and safety of employees and contractors on site, and building shared resilience with host communities.

Infrastructure Risk

The Philippines’ transmission network faces capacity constraints that limit reliable power delivery across the grid. For First Gen, this creates both an operational risk and a growth risk—existing plants may face dispatch limitations while new renewable projects may struggle to connect to the grid at all.

Risk Type: External

Capitals Affected and Direct and Indirect Impacts

- Financial—Dispatch limitations on existing plants and delays in connecting new projects reduce revenue and increase the cost of project development.

- Manufactured—Assets that cannot fully dispatch or connect to the grid are underutilized, eroding the value of First Gen’s portfolio.

- Human—Grid constraints require First Gen to develop capabilities such as contracting and overseeing the construction of dedicated transmission facilities—diverting organizational capacity from core business activities.

- Natural—When renewable generation cannot be fully dispatched due to grid constraints, the environmental benefit of clean power—reduced emissions and cleaner air—is not realized.

Stakeholders Affected by or Involved in Risk Management

- Customers—Grid constraints that limit dispatch from existing plants or delay new projects affect the reliability and availability of clean power supply that customers depend on.

- National Grid Corporation of the Philippines (NGCP)—As the transmission system operator, NGCP is the primary partner in identifying grid gaps and planning the upgrades needed to connect new renewable capacity.

- Regulators—The DOE and ERC set the framework for transmission planning and investment that determines how quickly grid constraints can be addressed.

Likelihood of the Risk Occuring: Likely

Magnitude of the Impact on the Company: Major

Time Horizon: Medium to Long Term

Effects on Strategic Objectives and Key Targets

- Grid constraints that limit dispatch from existing plants reduce generation output and affect revenue and financial performance.

- Delays in connecting new renewable projects slow the growth of First Gen’s clean energy portfolio and push back decarbonization targets.

- Customers in both the captive and contestable markets lose access to reliable clean power when grid constraints limit delivery.

- Grid constraints that First Gen cannot resolve alone reinforce why building public advocacy capability is a strategic priority.

Mitigation Measures

- Direct Coordination with NGCP—To minimize delays and ensure that transmission requirements are identified early, First Gen engages NGCP directly on system impact studies and grid connection timelines for existing and pipeline projects.

- Regulatory and Policy Engagement—Participating in technical working groups and policy consultations with the DOE, ERC, and other regulatory bodies advances grid development as a national priority and ensures that transmission investment keeps pace with renewable energy growth.

- Public Advocacy Capability—Building CEAL as a coordinated advocacy platform across the First Gen power group advances clean energy needs.

- Project Planning—First Gen builds grid access requirements into project development through two mechanisms: GRAC enforces project development discipline through its gate review system, ensuring teams have addressed transmission feasibility before capital is committed, and AMPD builds the processes and systems that embed this discipline into project management practice across the portfolio.

What These Measures Achieve

These measures reduce the exposure of First Gen’s renewable portfolio to grid constraints—protecting generation output, keeping project timelines on track, and ensuring that customers in both the captive and contestable markets can access the clean power First Gen produces. A well-functioning transmission network benefits all energy users, not just First Gen.

Fuel Supply Risk

Geothermal steam and river water are not fuels that can be ordered, stored, or substituted. They are governed by natural systems—reservoir dynamics underground, rainfall patterns above. For geothermal assets, the challenge is both geological and financial: steam production can decline over time, and the cost of exploration and drilling to maintain or expand capacity requires sustained capital investment with uncertain returns. Reservoir potential can be modeled—geologists use sophisticated subsurface analysis to estimate what lies beneath—but the actual steam yield is only known once a well is drilled and brought online. For hydroelectric plants, the fuel is rainfall and river flow. Output depends on how much water moves through the watershed—and climate variability makes that increasingly difficult to predict. El Niño cycles, which return every three to seven years in the Philippines, can suppress rainfall significantly across operating watersheds, reducing river inflow and generation output.

Reservoir conditions evolve naturally across all geothermal assets. At Leyte, declining plant availability has brought the asset to a decision point—one that requires weighing technical feasibility, capital requirements, grid reliability, and sustainable design principles before a path forward can be determined.

Risk Type: External

Capitals Affected and Direct and Indirect Impacts

- Financial—Steam exploration and drilling require substantial capital before the resource is confirmed. For operating geothermal assets, declining steam availability or quality reduces generation output and revenue. For hydroelectric assets, lower than expected water availability directly reduces generation output and revenue. Operating costs remain regardless of fuel availability and supply.

- Manufactured—Geothermal and hydro plants are long-life assets whose value depends on continuous generation. If steam or water supply falls short, plants operate below capacity and the productive value of those assets is not realized.

- Human—Managing reservoir behavior and water systems requires specialized expertise that is not readily available. First Gen’s ability to respond to fuel supply challenges depends on retaining or having sustained access to this capability.

- Intellectual—Decades of operating geothermal and hydro assets have produced reservoir models, drilling data, well data, and other site-specific knowledge. This institutional knowledge is the foundation for managing fuel supply risk.

Stakeholders Affected by or Involved in Risk Management

- Investors—Capital deployed in exploration and drilling may carry higher outcome uncertainty compared to other investments. Underperforming wells and declining asset output due to fuel supply issues directly affect returns on investment.

- Customers—Customers who have actively chosen renewable energy depend on First Gen’s geothermal and hydro capacity to deliver on that commitment. If fuel supply falls short, replacement power may come from non-renewable sources and may undermine their goals. For customers dependent on baseload supply, the risk is more immediate: reduced generation capacity means power supply disruption.

Likelihood of the Risk Occurring: Possible

Magnitude of the Impact on the Company: Significant

Time Horizon: Medium to Long Term

Effects on Strategic Objectives and Key Targets

- Fuel supply shortfalls reduce clean generation output. These also affect financial performance and put at risk First Gen’s ability to deliver on its regenerative partnerships.

- Prolonged uncertainty in Leyte delays capital decisions and puts baseload capacity at risk, slowing the realization of our clean energy ambition.

Mitigation Measures

- Resilient Asset Management (RAM) capability—First Gen is building RAM as a core capability to sustain generation from assets whose fuel supply is governed by natural systems.

- For Geothermal Steam Resource:

- Reservoir Management—Continuously monitoring steam and applying targeted reservoir interventions sustain steam supply and optimize extraction from existing wells. To ensure steam supply, drilling and non-drilling workovers are programmed. Addressing steam decline requires: scaling prevention initiatives, lower-impact distribution of reinjection, and targeted infill injection for pressure support.

- Well Development and FCRS Management—Employing comprehensive well development planning, improved well design and predictive modeling tools, intensive monitoring of production lines, debottlenecking activities, and fortifying vulnerable wells and surface facilities.

- Leyte Study—Determining the responsible path forward for the Leyte complex through EDC-initiated comprehensive feasibility studies evaluating options for the aboveground facility under evolving reservoir conditions.

- For Hydroelectric Water Resource:

- Water Availability Monitoring—Conducting studies to track water availability across hydro assets and future project sites, informing operational and investment decisions.

- Watershed Management—Implementing watershed management programs close to sites to help sustainably manage land and water resources.

What These Measures Achieve

These measures protect the fuel supply critical for First Gen’s renewable generation. Sustaining steam and water supply keeps existing assets productive, preserves the baseload renewable capacity the Philippine grid depends on during the energy transition, and maintains First Gen’s commitment to deliver clean, reliable energy to customers who have chosen it for that purpose.

Financial Risk

Global financial markets in 2025 remained volatile, shaped by persistent geopolitical tensions and trade uncertainty. For First Gen, the more immediate exposure was in foreign exchange: the peso moved across a wide range during the year, from PHP55.35 to PHP59.41 against the dollar. The volatility in currency markets and broader uncertainty in global capital markets continues to affect the cost and timing of financing for new renewable energy projects.

Risk Type: External

Capitals Affected, Direct and Indirect Impacts

- Financial—Peso volatility and uncertainty in global capital markets affect the cost of foreign-denominated loans and project financing.

- Manufactured—Financing uncertainty may delay the development and construction of new assets, slowing First Gen’s portfolio growth.

Stakeholders Affected by or Involved in Risk Management

- Investors—Peso volatility and uncertain financing conditions affect project costs and returns, directly influencing First Gen’s financial performance and profitability.

Likelihood of the Risk Occuring: Possible

Magnitude of the Impact on the Company: Significant

Time Horizon: Medium to Long Term

Effects on Strategic Objectives and Key Targets

- Failure to monitor and anticipate drastic movements in foreign exchange and interest rates may put First Gen in a tighter financial position, constraining the capital available to fund new renewable energy projects and slowing the pace of growth.

- When project development slows, so does First Gen’s ability to serve customers who need us as a partner in their energy transition.

Mitigation Measures

- Cash Flow and Debt Management—Close monitoring of cash flows and major expenses. Deliberately making loan availments, reserved for strategically important investments. Actively pursuing a deleveraging program will reduce overall debt exposure.

- Interest Rate Risk Management—Maintaining a mix of fixed- and floating-rate loans to balance cost certainty against flexibility as rates move.

- Liquidity Risk Management—Prepaying loans where possible and refinancing bulky maturities to smooth and extend the repayment profile reduces concentration risk.

- Foreign Exchange Risk Management—Maximizing natural hedging where revenue and cost structures allow. The Finance and Treasury Group monitors FX rates continuously to identify hedging opportunities. Senior Management is regularly informed of FX exposure and mitigation plans.

- Partnership Development—Exploring partnerships for new projects to reduce First Gen’s solo capital exposure and distribute financing risk.

- Capital Allocation Governance—The Gate Review and Approval Committee (GRAC) ensures that capital deployment decisions are subject to structured review.

What These Measures Achieve

Taken together, these measures protect First Gen’s financial flexibility: the capacity to fund projects, manage obligations, and pursue the clean energy ambition even as global markets remain volatile. Reducing high-interest debt and extending repayment profiles strengthens the balance sheet. Active forex monitoring limits the damage from peso volatility. Disciplined capital allocation ensures that financing goes where it creates the most strategic value.

Cybersecurity Risk

The increasing digitalization and convergence of Information Technology (IT) and Operational Technology (OT) systems have improved efficiency across power generation, supply chain, and customer operations—and increased exposure to cyber threats. A successful cybersecurity incident can disrupt service continuity, compromise safety, and erode our stakeholders’ trust.

Risk Type: Internal and External

Capitals Affected, Direct and Indirect Impacts

- Intellectual Capital—Unauthorized access, data breaches, or system compromises may result in the loss, corruption, or misuse of sensitive information, proprietary systems, and operational knowledge critical to business performance and decision-making.

- Social & Relationship Capital—Cybersecurity incidents may erode trust among customers, regulators, business partners, and other stakeholders, potentially leading to increased regulatory scrutiny, loss of stakeholder confidence, and lasting reputation damage.

- Financial—Direct financial losses may arise from fraud, incident response, remediation, regulatory penalties, and business interruption. Reputational damage compounds this—affecting investor confidence, customer retention, and access to capital.

- Human—Employees, contractors, and customers may face personal data exposure, operational disruptions, and safety risks. Incident response places additional demands on employees managing it.

- Manufactured—Cyber incidents affecting IT and OT systems may disrupt power generation and delivery, threatening the reliability and continuity of operations.

Stakeholders Affected by or Involved in Risk Management

- Customers—Service disruptions and data exposure directly affect customers who depend on First Gen for power and trust it with their information.

- Employees and Contractors—Personal data exposure and operational disruptions affect the people running First Gen’s systems. Incident response places additional demands on employees and contractors.

- Regulators—An incident triggers heightened compliance scrutiny, reporting obligations, and potential sanctions.

- Investors—Incidents that disrupt operations or damage reputation affect financial performance and access to capital.

Likelihood of the Risk Occuring: Possible

Magnitude of the Impact on the Company: Significant

Time Horizon: Short to Long Term

Effects on Strategic Objectives and Key Targets

- A successful cybersecurity incident can disrupt operations and trigger penalties, directly undermining First Gen’s ability to deliver reliable clean energy.

- For a company building long-term customer partnerships, reputation damage from a high-profile breach may have significant long-term effects.

Mitigation Measures

- Layered Security Controls—Preventive, detective, and corrective controls

- Cybersecurity Governance—Oversight and risk management processes at the appropriate organizational level

- Continuous Monitoring—Ongoing monitoring of systems and networks to identify and respond to threats

- System and Network—Secure system and network design installed

- Employee Awareness—Cybersecurity awareness programs conducted across the organization

What These Measures Achieve

Together, these measures strengthen the company’s security by improving threat detection, reducing vulnerabilities, enhancing access controls, and building organizational awareness needed to lower both the likelihood and impact of a cyber incident.

Opportunities Shaping Our Next Risk Profile

The forces pressuring First Gen are the same forces creating opportunity for it. A world demanding cleaner energy, opening markets to competition, and making carbon emissions costly is the world First Gen has been preparing for—through the portfolio choices and governance structures described in the Strategy section. Managing the risks described in this section is what keeps those opportunities within reach. The Outlook section makes the case for the enabling conditions that would accelerate these opportunities.

RETAIL MARKET EXPANSION

The opening of RCOA Phase 4 in June 2026 brings approximately 12,000 medium-sized enterprises into the contestable market, each newly able to choose their electricity supplier. The opportunity is real, as is the execution risk of pursuing this. First Gen has been preparing for both—from building the Revenue Office and Customer Engagement Office to acquiring Pi Energy and integrating its platform. (See Choice #2, Strategy Section)

RENEWABLE PORTFOLIO ADVANTAGE

As the cost of carbon emissions rises regionally and globally, renewable generation gains ground. For First Gen, geothermal and hydro assets provide baseload reliability, while solar, wind, and distributed solutions add scalable capacity—together positioning First Gen to serve customers seeking decarbonization and energy security. (See Good Choice #1: Decarbonize our Portfolio)

Both opportunities depend on enabling conditions that First Gen cannot build alone.