BUSINESS ENVIRONMENT: AT A GLANCE

The Philippine energy transition is shaped by policy direction but constrained by gaps in implementation.

Philippine Energy Challenge.

Progressive climate and energy laws, including the RE Law and coal moratorium, set the direction. Coal accounted for approximately 57 percent of power generation as of the first half of 2025—the first meaningful decline in years, yet still dominant.1

Transition Gap.

Renewable energy has reached approximately 32 percent of the Philippines’ total power installed capacity as of mid-2025,1 yet its share of annual power generation has remained at approximately 22 percent for the past three years.2 Coal’s recent decline was absorbed by natural gas, not by renewable generation.1

Five Forces.

First Gen operates within a business environment shaped by tensions across climate and nature risks, policy design and market implementation , customer complexity, stakeholder relationships, and capital market expectations—each examined in the sections that follow.

The Philippine Energy Challenge: Bridging the Gap Between Law and Reality

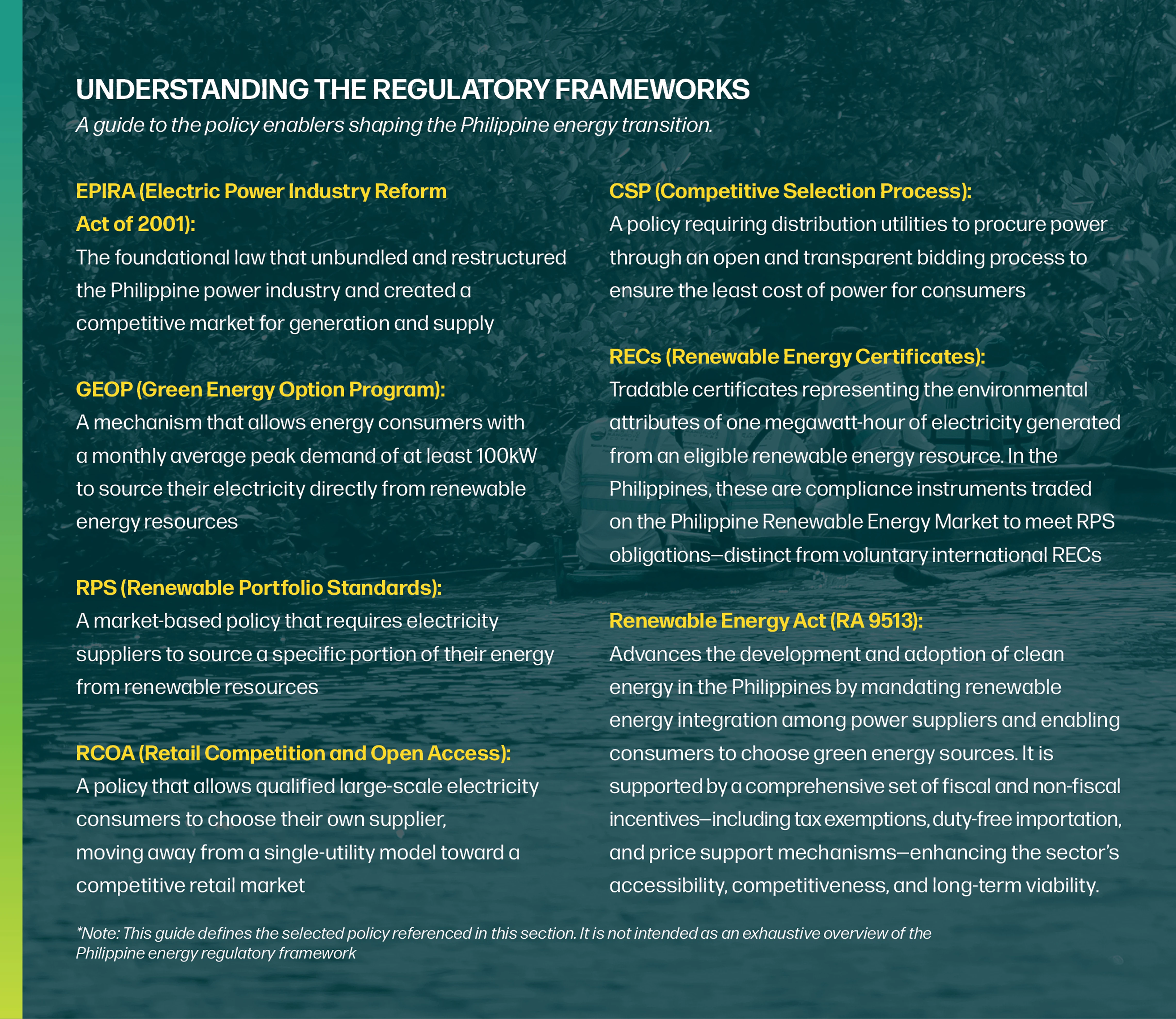

The Philippine power sector is operating under a structural tension between policy ambitions and its operating reality. On paper, the country has established one of Southeast Asia’s more comprehensive renewable energy policy frameworks, supported by commitments under the Paris Agreement and reforms such as the Electric Power Industry Reform Act of 2001 (EPIRA) and the Green Energy Option Program (GEOP).

International observers have taken note of the Philippines’ policy ambition. BloombergNEF’s Climatescope 2024 ranked the Philippines the second most attractive emerging market for renewable energy investment globally,3 and the World Bank approved a First Energy Transition and Climate Resilience Development Policy Loan in March 2025.4 These recognitions reflect the Philippines’ policy framework and the continued confidence of international institutions in its energy transition direction.

Coal supplied approximately 57 percent of power generation as of the first half of 2025, down from ~62 percent as of 2024— the first meaningful decline in years driven largely by a shift to natural gas.1 Renewable energy has reached approximately 32 percent of total Philippines power installed capacity as of mid-2025. Yet its share of annual power generation has remained at approximately 22 percent for the past three years. The data suggests the infrastructure is heading in the right direction, but electricity used by customers remains largely fossil based.2

How eligibility rules are structured, how compliance obligations are met—and whether those mechanisms translate into actual clean generation—these remain the unresolved tensions between the policy ambition and outcomes.

The Forces Shaping Our Business Environment

First Gen operates inside this tension. Our portfolio spans geothermal energy—the Philippines’ most established renewable baseload—and an expanding slate of renewable assets being built for the evolving market. We are not observers in this energy transition; we aspire to lead it.

The pace at which implementation catches up with policy ambition, the rules that govern how clean energy reaches customers, the capital that flows toward credible transition plans—these directly determine the conditions under which we operate, invest, and grow. Five forces define that environment.

Earth: Climate and Nature

Climate volatility impacts everyone and everything involved in building and operating energy infrastructure. Intensifying weather events and ecosystem degradation disrupt asset operations, negatively impact host communities and employees, and drive resilience-related capital requirements. Asset performance is influenced not only by engineering design but by watershed health, ecosystem stability, and broader natural systems.

Industry: Policy Design and Market Implementation

The Philippines has adopted comprehensive renewable energy frameworks, yet policy signals are moving in different directions, simultaneously. Under the Renewable Portfolio Standards, obligated parties can satisfy compliance by purchasing Renewable Energy Certificates from existing eligible facilities—which means they can meet their RPS obligation without directly sourcing power from clean generation.10 With REC prices regulated at modest levels, the incentive for new renewable investment is limited. The coal moratorium—designed to halt new greenfield coal development—has been qualified by exemptions, raising the question of whether the policy signal against new coal remains intact.11

At the same time, enabling mechanisms are being built. The Philippine Geothermal Resource De-Risking Facility—a USD170-million program launched by DOE and the Land Bank of the Philippines in December 2025, funded through an ADB sovereign loan—directly addresses one of the most persistent barriers to geothermal development by co-sharing early exploration costs with investors.5

The result is a policy environment that accelerates and impedes the transition at the same time. How these dynamics shape participation across corporate, enterprise, and household segments is detailed in Making Clean Energy Easy to Choose.

Customers: Complex Needs

The Philippine electricity market has not completed its transition to open competition. Twenty-five years after the enactment of EPIRA, captive and contestable customers coexist under different rules and a different set of available choices. Distribution utilities and electric cooperatives have long been First Gen’s primary off-takers—requiring bulk power, standardized contracts, regulated relationships. Today, corporate accounts navigating Scope 2 emissions reporting, medium enterprises entering retail competition under RCOA, and households evaluating distributed generation are all entering the picture—each with different needs, different decision criteria, and different pathways to participation. Serving this range of customers requires a wider set of capabilities, tools, and systems.

Co-Creators: Employees, Communities, and Partners

Project execution depends on sustained alignment with communities, employees, and supply chain partners operating under their own climate and capability pressures. Managing geothermal assets, expanding into new markets, and preparing for a retail-oriented domestic landscape require continuous technical depth, operational discipline, and community trust. The degree of that alignment directly determines whether projects are delivered on time, at planned cost, and whether assets perform over the long term.

Investors: Transition Credibility and the Cost of Capital

Global capital is moving toward the energy transition, but investors are increasingly selective about where it goes. Research covering 3,028 listed companies found that firms initiating disclosure of environmental performance metrics enjoy a measurably lower cost of equity capital—a relationship that strengthened after the Paris Agreement and that holds particularly in emerging markets.6

A separate survey of 1,400 senior energy transition executives across 36 countries found that regulatory and policy risk ranks as their top barrier to deploying capital.7 Those policy risks are what investors price. Perceived risk drives financing cost; credible transition plans and policy consistency lower it.

For a power company, the cost of capital will likely depend on the credibility of its transition commitments and the quality of its disclosures.

Cost of capital also depends on the environment it operates in—investors price policy risks at the country level as well. A Philippine energy transition supported by clear and stable policy frameworks strengthens the investment case for the entire sector.

Operating in a World of Extremes

Climate risk has moved from abstract projection to daily operational reality. Weather volatility now tests the physical limits of infrastructure and reshapes the conditions under which energy systems must function. Super Typhoon Carina’s record 471mm rainfall in Quezon City and Severe Tropical Storm Kristine’s subsequent 528.5mm deluge in Daet, Camarines Norte were not isolated events.8 They illustrate the growing intensity and unpredictability of climate exposure confronting asset operators across the country.

Maintaining resilience requires more than minimizing harm. Long-term asset performance is linked to watershed stability, forest cover, and broader ecosystem health. Physical infrastructure and natural capital are interdependent systems. The durability of one depends on the integrity of the other.9

The implications of these climate exposures—including their connection to natural capital and enterprise risk— are addressed in the Natural Capital section and the Risk Management and Opportunities section.

Making Clean Energy Easy to Choose

Across the country, willingness to participate in the transition is evident. Customers—corporate, commercial, and residential—are increasingly attentive to cost stability, emissions reporting, and energy security.

Large corporations navigating Scope 2 reporting assess the difference between bundled renewable supply under GEOP and unbundled Renewable Energy Certificates. Medium-sized enterprises anticipating eligibility under RCOA Phase 4—expected to expand supplier choice to approximately 12,000 additional enterprises by June 2026—face decisions about pricing, contract terms, and risk exposure. As of January 2025, more than 2,100 of roughly 3,600 eligible end-users had already switched suppliers, reflecting meaningful consumer engagement.12

Households and small businesses have fewer options beyond their local Distribution Utility or Co-Operative, net metering through behind the meter solar installation being one. Recent reforms have begun to address this: ERC Resolution No. 15 Series of 2025 introduced indefinite banking and rollover of export credits, and a DOE supplemental policy in October 2025 now allows net metering to own and trade their RECs. DOE also streamlined permitting processes in early 2026. The direction is right. Making participation economically worthwhile for every customer segment is work in progress.13

The People Behind the Transition

Delivering on the transition will demand more than capital and policy. It demands sustained effort—technical, organizational, and relational—across decades.

Managing renewable assets under evolving natural conditions, scaling a renewable portfolio, and serving a more complex customer landscape require continuous technical upskilling, operational discipline, and stakeholder management. Transition execution spans engineering, commercial structuring, regulatory navigation, collaborative cultures, and community engagement.

Project outcomes increasingly depend on partnership rather than permission. Host communities, supply chain partners, and employees each carry climate and capability pressures of their own. Alignment around long-term asset resilience and regenerative practices is therefore not aspirational—it is operationally necessary.

More information on these interdependencies may be found in the Strategy section, Financial Capital section, Manufactured Capital section, Natural Capital section, Human Capital section, Intellectual Capital section, and Social and Relationship Capital section.

The Transition Ahead

The Philippine energy transition is advancing within structural constraints, evolving implementation rules, physical climate realities, and shifting capital expectations.

Clarity about exposure, discipline in execution, and consistency in long-term positioning define whether progress accelerates in practice as well as in policy.

1Independent Electricity Market Operator of the Philippines (IEMOP), H1 2025 generation data, as reported in Reuters, “Philippines set for first coal power decline in 17 years amid rising LNG use,” July 22, 2025.

2Department of Energy Philippines, “Summary (Electricity Consumption, System Demand, Generation, Installed and Dependable Capacity), 2003–2024; Department of Energy Philippines, Secretary Sharon Garin as reported by Philippine News Agency, “DOE confident of hitting RE target,” November 21, 2025 ..

3BloombergNEF, Climatescope 2024, 2024.

4World Bank, “Philippines Energy Transition and Climate Resilience Development Policy Operation,” March 2025.

5BusinessWorld, “DOE, LandBank to launch ₱10-B de-risking facility for geothermal developers,” December 16, 2025

6Gao, Yumeng, Benjamin C. Herbert, and Lionel Melin, “The ESG Disclosure Premium,” Yale University / Arvella Investments, July 2024, https://ssrn.com/abstract=4935848

7KPMG International, Energy Transition Investment Outlook: 2025 and Beyond, 2024, https://kpmg.com/xx/en/our-insights/esg/energy-transition-investment-outlook-2025-and-beyond.html

8PAGASA. (2025). Tropical cyclone preliminary report: Super Typhoon Carina (Gaemi). Marine Meteorological Services Section, Weather Division. ; PAGASA. (2025). Tropical cyclone preliminary report: Severe Tropical Storm Kristine (Trami). Marine Meteorological Services Section, Weather Division.

9First Philippine Holdings, “Nowhere to Go: Net Zero.”

10Department of Energy (Philippines), “Renewable Portfolio Standards Eligibility List,” February 2025.

11Department of Energy Philippines, Coal Moratorium Advisory, December 22, 2020; Department of Energy Philippines, Advisory on the Non-Coverage to the Coal Moratorium Policy, effective October 14, 2025

12Energy Regulatory Commission data on RCOA switching, January 2025.

13ERC Resolution No. 15, Series of 2025 (Net Metering Rules, banking and rollover of credits); DOE Supplemental Policy, October 2025 (REC ownership and trading); DOE Department Circular, February 2026 (multi-site net metering and permitting reforms).